Inflation: is Bank of England criticism fair?

The barrage of briefings over the weekend from senior Conservatives against the Bank of England and its Governor, Andrew Bailey, over the Bank’s role in the inflationary crisis that is buffeting the UK economy seem to have little to do with economics and a lot to do with politics. It will certainly make for an interesting session of the Treasury Select Committee today.

Is the criticism fair?

Some of it can be easily dismissed.

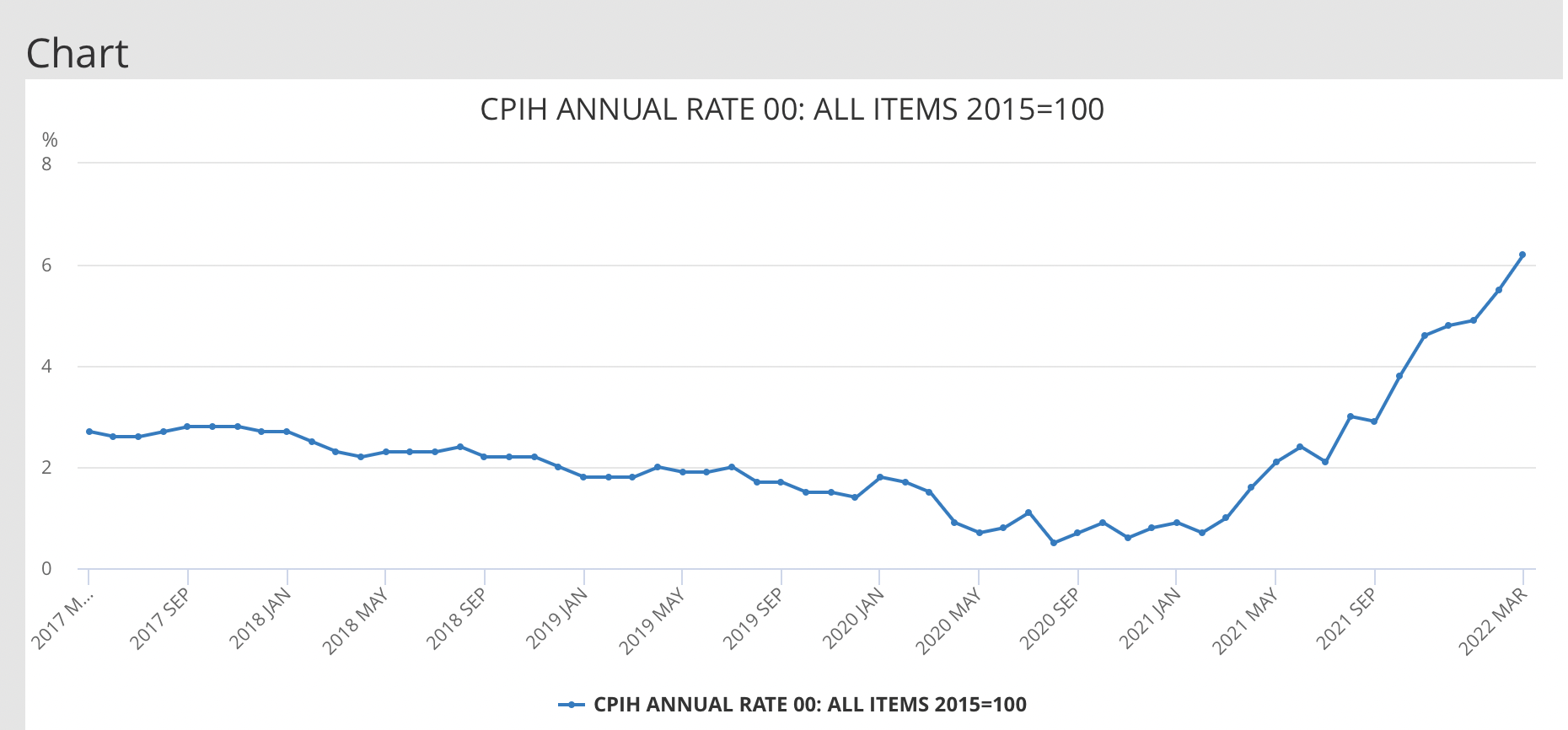

If, as The Sunday Telegraph reported, a Cabinet minister really said of the BoE “It has one job to do — to keep inflation at around 2 per cent — and it’s hard to remember the last time it achieved that target” then it is hard not to despair. Is there really someone sitting round the Cabinet table whose memory about such key economic data really does not extend further back than nine months? Inflation was just 2.1% last July, having been below 2% all the way through the long months of pandemic lockdowns (see graph).

Central bankers are certainly in difficult position as they have boxed themselves into a monetary policy corner in the wake of the Global Financial Crisis, now over a decade ago. The slashing of interest rates and the pumping of billions into financial markets via the quantitative easing programmes saved the financial system from collapse, but many economists have been warning for a few years that the banks were being too slow to move back to normality so that they would have room for manoeuvre when the next crisis struck.

Inflation has caught them on the hop and some have been complacent in their analysis and response. Others have been wiser.

Jerome Powell, chair of the US Federal Reserve, was striking a gloomy note in the late autumn. He said using the word “transitory” in conversations around inflation should be retired, when he appeared before the US Senate’s Committee on Banking, Housing, and Urban Affairs. For Powell inflation was being driven by a range of factors, the push of rising raw material and energy prices and the pull of consumer demand: “Pandemic-related supply and demand imbalances have contributed to notable price increases in some areas. Supply chain problems have made it difficult for producers to meet strong demand, particularly for goods. Increases in energy prices and rents are also pushing inflation upward.” And this was before Russia launched its assault on Ukraine and China effectively closed one of its largest ports.

Powell’s assessment was not shared by European Central Bank president Christine Lagarde who told a Reuters event a few days later that inflation was transitory, playing down fears that it would continue to rise well into 2022: “I see an inflation profile that looks like a hump,” Lagarde said. “And a hump eventually declines. We are firmly of the view, and I’m confident, that inflation will decline in 2022.” The ECB still hasn’t made a move of interest rates, suggesting Lagarde is stubbornly sticking to this belief, despite the powerful global trends to the contrary.

Bailey, an instinctively cautious man, positioned himself somewhere between these two views when last appeared before the Treasury Select Committee in December. He was not shy about the problem inflation poses but offered few firm commitments on interest rate policy: “I’m very uneasy about the inflation situation. I want to be very clear on that. It is not, of course, where we wanted to be, to have inflation above target.”

Central banks are fearful about being manoeuvred into a situation where interest rates are increased but inflation does not respond. This is a seminal moment for them as one of the cornerstones of monetary policy in the 21st century, controlling inflation through interest rates, is put to its first real test. The policy has worked because most inflationary – and deflationary – pressures over the last 25 years have been caused by fluctuations in consumer demand – the pull factors.

If central banks raise interest rates or curtail their bond purchase programmes and the impact that has on demand is minimal, people will start to lose faith in their ability to control inflation. The longer higher rates of inflation prevail, the more they become part of a new normal which could add fuel to the push factors by unleashing demands for higher wages and making regular price increases more acceptable. the wage-price spiral that dogged the 1970s.

If you accept that inflation is being driven by push factors rather than surplus demand then it points to a need to return to economic management through fiscal policies and that turns the spotlight on governments, which gives you a clue as to why Tory MPs are looking to put Bailey on the spot. The government seems to be like a hapless rabbit caught in the spotlight. It is doing next to nothing to address the powerful push factors such as rising energy prices and food price increases. Indeed, it has added to the cost-of-living pressures by increasing National Insurance (although this will not show in inflation data).

The problem for Mr Bailey today is that he will not feel it is his job to turn the spotlight back on the government – that would be political dynamite – but, at the same time, he does not want to admit that the monetary weapons in his armoury are potentially ineffective against the powerful push factors driving inflation.

It will be interesting viewing.