Now the run-up to the local elections in England and to the Scottish and Welsh Parliaments on 7 May is underway, the speculation about the potential impact on the leadership of the Conservative and Labour parties is already bubbling away.

It is tediously familiar to anyone who follows politics in this country. Lose a few council seats and reach for the panic button. This has been a major factor in both parties changing leader with whirlwind frequency over the last decade. This hasn’t made for better politics and certainly not better government.

As we approach polling day, question marks hang over both Kier Starmer and Kemi Badenoch. Certainly in the Labour Party, rivals are already jostling for position should the results come in at the more catastrophic end of the prediction spectrum. Badenoch will also be watching the results with one eye cast back over her shoulder in case her leadership is threatened, although with her main rival, Robert Jenrick, sailing off to join Reform she looks slightly more secure.

It wasn’t always like this.

In the late 1960s, the Labour government was deeply unpopular as inflation started ticking up, the pound had been devalued (then a big issue), new charges were introduced for prescriptions and immigration was becoming a toxic issue, especially after Tory MP Enoch Powell’s notorious ‘rivers of blood’ speech in April 1968.

The local election results that year were a disaster for Labour. They took a hammering across the country, including losing all their seats in Birmingham. 1969 was even worse with only two London boroughs – Southwark and Tower Hamlets – remaining safely in Labour hands and Labour in Newham relying on the casting vote of an unelected Alderman to stay in office.

Yet, Harold Wilson remained Prime Minister and led them into the 1970 General Election, which the Tories narrowly won. Still, Wilson did not go, instead leading Labour back into government in the two elections of 1974.

This doesn’t mean there wasn’t a wobble, at least in 1968.

The day after the 1968 elections, the proprietor of the Daily Mirror Cecil King waded in with a ferocious attack on Wilson, hung more on the peg of the financial crisis than poor election results but it prompted some serious head-scratching among the Labour elite, according to those prolific diarists of that era Richard Crossman and Tony Benn.

Writing on Saturday 11 May 1968, Crossman summed up what he saw as the position Wilson was now in:

I don’t dispute for a moment that Cecil King’s attack has temporarily strengthened Harold’s position a great deal. Nevertheless I have no doubt that this week has seen another move in the direction of a new leadership. I think the party will sooner or later insist that whether it’s going to win the next election or at least lose it honourably (which is the least we can hope) it will have a new leader, unless Harold can show a power of retiring into the background and letting leadership headed by Roy [Jenkins] and Barbara [Castle] give the inspiration which he can’t give. I think all that will happen but it can’t happen when our press lords start ordering the party about.”

That proved a brief wobble as no leadership challenge emerged, not least because the most obvious candidate, Roy Jenkins, was considered by many to be too aloof and patrician and did not allow himself to be manoeuvred into a position where he could have been seen as a viable alternative.

With the results the following May just as bad, leaving Labour in control of just 28 out of 342 borough councils in England and Wales, one might expect to find a rising tide of discontent with Wilson’s leadership. If this May looks anything like that for Labour, Starmer will be struggling to keep his job.

Nothing of the sort happened in 1969.

The day after the local elections, Labour held an eight hour meeting of its then all-powerful National Executive Committee at 10 Downing Street. Neither Crossman or Benn record any serious criticism of Wilson, although there were plenty of grumbles about public expenditure cuts and increased prescription and dental charges.

Starmer and Badenoch might find themselves wishing for a return to those more policy- rather than personality-focused days after 7 May.

Perhaps we could all do with a little more stability at the top of our political parties.

• Wilson chose his own departure, surprising everyone by standing down as Prime Minister in March 1976, to be succeeded by Jim Callaghan

David Bland, who has passed away at the 85 after a long illness, revitalised the Chartered Insurance Institute during the 1990s when he led it as director-general. In doing so, he took insurance education into a new era.

He came to the role after an already illustrious career in academia, having studied and taught economics and economic history at the University of Sheffield for over 20 years, serving as Dean of Social Sciences and then Pro-Vice Chancellor between 1984 and 1988.

He arrived at the CII in 1989 when the organisation was at a crossroads. Its examinations were looking outdated and the rapid growth of the emerging financial advice sector was passing it by. He also inherited an increasingly bitter dispute about how the newly created title of Chartered Insurer was going to be applied, with many senior members of the profession being denied it because they were granted Fellowship before examinations were introduced in 1963. His almost immediate decision to push through their eligibility for the Chartered title won him many valuable allies among the more influential members of the profession.

This gave him the mandate he needed to overhaul the examinations, bringing in new qualifications for financial advisers and other staff who were not going to aspire to full professional qualifications. This came just at the right time, and the CII enjoyed a new lease of life – and a considerable boost to its finances – by examining tens of thousands of staff who would not previously have come into its orbit but who now had a suite of respected qualifications they could aspire to. This also suited the new era of more prescriptive regulation which was then dawning.

He won support for these major changes through the intellectual rigour he brought to the role and the always admirable clarity with which he advocated the changes, often winning over a previously sceptical membership. He was deservedly honoured with an OBE in 1998.

In my various roles at what was then Post Magazine, I covered all these debates in great detail and came to know David well as the critical friend our respective roles demanded.

Return to academia

After leaving the CII in 2000, he returned to academia as head of the business school at the University of East London for a few years before taking on various roles as a consumer champion for the water and postal services sectors. He remained a prominent figure in the insurance market, however, writing several books including Principles and Practice of Insurance, which was eventually published in 14 languages.

He took on major roles as President of the Insurance Charities (2002-03), Master of the Worshipful Company of Insurers (2006-07), Master of the Worshipful Company of Firefighters (2010-11) and as a long-serving Churchwarden at St Michael’s, Cornhill.

It was in his capacity as the incoming President of the Insurance Charities that he invited me to lunch at the Athenaeum Club. I had already helped them with some of their marketing and communications activities and had recently become a trustee.

The two Davids

We both knew that one of the biggest challenges the organisation faced was the urgent need to simplify the complex mix of legacy charities that sat under its relatively recent marketing banner of The Insurance Charities. There was a Benevolent Fund and an Orphans’ Fund (the industry had once wanted to build its own orphanage), as well as a couple of large personal legacies separately managed. The terms of reference of these all dated back to before the Second World War and were feeling increasingly restrictive, hampering the ability of the organisation to meet the new demands being placed on it.

Sorting this out was not going to be easy and, knowing the speed with which the Charity Commission worked, was definitely going to take more than one year, the term of office of a President.

Our solution devised over that lunch was simple: I would succeed David as President and our shared objective would be to deliver a merger of the underlying charities and a new constitution in two years. That we did, one David quietly replacing the other halfway through that process.

We kept in touch over the years and he did me the honour of asking me to review some of his books, always a joy as well as an intellectual challenge.

He was a great servant of economic education, the insurance industry and the Livery movement.

Requiescat in Pace.

The long-expected confirmation that the UK will not include financial services in its tentative talks about closer alignment with European Union, our largest trading partner, shows we have learnt little from the fraught relationship we often had with the EU when we were members. The constant striving for British exceptionalism often soured and weakened our position with the bloc. It will do the same again.

Brexit has damaged the UK economically. Whatever data you look at the story is depressing.

The Office for Budget Responsibility has consistently said that GDP is 4% lower as a result of breaking with the EU in the hardest of hard Brexits. The US National Bureau of Economic Research recently went further, suggesting the damage could be in the region of 6% to 8%. Services exports – including financial services – have been estimated to be 4% lower due to Brexit.

We clearly need to look at how we can repair this damage and start rebuilding our trading relationship with the EU is essential. It should be central to the government’s much proclaimed growth agenda. The easiest and most obvious routes are by rejoining the Customs Union and the Single Market. Leaving these was not on the Brexit referendum ballot paper in 2016. They were the misguided choices of a Conservative government striking ever more macho poses over Brexit to the lasting detriment of the country.

The government is pushing for closer alignment with EU rules in some areas, such as food standards and animal welfare, while now ruling out financial services. But why should the EU accept this return of British exceptionalism? Why should it allow us to pick and choose? Does that really put us in a strong position? Surely, it will just allow the EU to pick which areas will benefit it most, often that might be a mutual benefit but where it sees no benefit to its member states it will just say no.

Struggle to justify separate UK regulatory regime

While there are inevitably voices raised in favour of maintaining an independent regime for UK financial services, they struggle to demonstrate a credible justification. They cite an increase in stock market flotations as one of the key uplifts but that is a worldwide trend.

On the debit side, there is the increased costs imposed on any financial business looking to service European clients. Gone is the passporting regime. They have had to establish new well-staffed offices in Europe. The products – such as insurance cover for European clients – have to comply with the requirements of the local regulators which are all derived from the EU rulebook. Ironically, in many areas the EU’s financial services regulatory regime was largely shaped by the British, especially in the run-up to the creation of the Single Market in 1992.

Then, there has been the cost and time expended on creating an alternative UK regime. When you look at the outcomes across different areas of financial services you really have to ask: “was it worth it?”. The changes are often little more than cosmetic, maybe occasionally benefitting firms purely trading in the UK but doing nothing for the international businesses that have been the traditional powerhouses of the City. The scrapping of the cap on bonuses is sometimes touted as a benefit, helping us win the global war for talent in the sector. That is a dubious claim. More serious is the impact it will have on wealth inequality which, in turn, will inhibit economic growth and improvement in productivity. Offset against that is the limitations on free movement which now present a barrier to talented young people wanting to move to the UK.

The City of London and its financial services sector are still making significant contributions to the UK economy, more despite Brexit than because of it. How much bigger and more vibrant would the sector be if it could throw off the shackles of Brexit. They are the inhibitors to greater success, not the imagined restrictions of having to trade within the carefully crafted rules of our largest trading partner.

Let’s be honest: Brexit is broken and it needs boldness to fix it, not the blinkered exceptionalism of the past.

Hardly a day goes by without artificial intelligence making headlines with claims of fresh advances, often accompanied by warnings of the unspecified dystopian future it might be heralding. Its progress is relentless, its potential ever expanding and its shortcomings ever more visible to those who have their eyes open.

It often seems that all around AI there is a battle raging where powerful commercial interests, political forces and national governments slug it out, contemptuously dismissive of those who might be innocent casualties – such as creatives watching the value of copyright brutally eroded – or who urge caution, even daring to utter the R word – regulation.

Many have concerns about where the AI revolution might lead and how it will change society but it often seems few can be really bothered to get to grips with its implications. It is important that we do, for we all have a stake in its development and the journey it could take society on.

That’s why I was pleased to be able to arrange a briefing on AI for the UK Section of the European Journalists last week. It turned out to be illuminating, worrying but also reassuring.

The discussion was led by Michael McNamara, an independent Irish MEP and co-chair of the European Parliament’s Working Group on the Implementation and Enforcement of the AI Act, and Graham Lovelace, strategist and consultant on AI, especially its impact on media. Both offered insights into how AI is developing and, crucially, how it might be regulated so that its potential benefits outweigh the downsides that many of its more blinkered advocates constantly gloss over.

• My detailed report of the meeting is available on the AEJ-UK website.

It was very wide-ranging but there are two key takeaways for me from it.

The first is the danger highlighted by Graham Lovelace of journalists and the media of lazily slipping into bad habits in their use of AI, especially using it to generate content. He highlighted several uses of AI that are already commonplace, such as using it to suggest headlines, crunch vast datasets to expose trends, transcribe long interviews or meetings, translate into multiple languages or generate the meta data needed for websites, the latter a dull task definitely better automated in his view.

But some are already sliding down a slope towards a more indiscriminate use of AI, using it to research stories, gradually placing too much faith in responses, and then perhaps letting it write the stories. It is happening. But even those using it to do this acknowledge that accuracy cannot be guaranteed. Lazily recycling content from AI will lead to the creation of “AI slop” where fake content is given greater validity by being repeated. Once journalists allow that to happen, trust will evaporate.

Where will this lead, he asked? It will dull the creative spark and the ability to think critically will decline.

The answers, he suggested, are simple but potentially elusive. Use AI at the end of a creative process, not at the beginning. And label it. Be honest with readers. And independently research, check and challenge every step of the way.

Transparency and honesty

This was also urged as part of the solution by Michael McNamara, who said that not identifying the use of AI is potentially dangerous for politicians as well as journalists. Asking AI to write a speech is every bit as dangerous as asking it to write a news story. Transparency and honesty about its use are essential.

He was also reassuring in his explanation of the robust measures the European Union is looking to put in place to ensure the responsible use of AI. He admitted that not all of this is perfect, citing the current stand-off over copyright as a messy compromise. This will be a crucial fight because what AI developers are doing at present in indiscriminately scraping the web for content is nothing short of theft, said Graham Lovelace.

On this and other threats from Ai to privacy, personal data and its ability to generate fake news, audio and video, it is clear the EU is determined to face up to the power of those big tech interests to whom any regulation is an anathema and put some sensible protections in place. He was hopeful that the UK might follow suit, praising the work being done in the House of Lords by Baroness Kidron.

Yes. AI is here to stay. Its use will grow and benefits will flow from that but it is far from perfect, which is why using it with caution is a prerequisite of responsible journalism – and being open and transparent about its use is essential.

• The main image has been generated by the Adobe Stock library using AI

Reform UK’s sustained rise in the opinion polls and local elections can no longer be ignored by those who hope that Farage and co never get the opportunity to put their distorted, divisive, ignorant policies into action by playing a part in the government of this country.

As the drip, drip of detail seeps out from what passes for policy making machinery in Reform, we can see its agenda is being shaped by the MAGA (Make America Great Again) agenda being relentlessly pursued by President Trump. It is surprising just how little detailed scrutiny this is being subject too.

This seems especially true of financial services. Last month at Reform’s conference we heard the start of Nigel Farage’s assault on the current regulatory regime for financial services. This featured a pledge to scrap much of what was put in place after the global financial crisis. It included a strong commitment to what Reform is labelling as “self-regulation”, perhaps involving the complete abolition of the Financial Conduct Authority.

This was followed up by a more specific pledge to abolish the FCA from Aaron Banks, founder of the Leave.EU campaign and a former insurance broker close to Farage. In an interview with the business publication Insurance Age, he said the FCA and the Solicitors Regulation Authority should both be abolished. He said nothing about how the self-regulation would replace them would work.

Last week, Farage unveiled another facet of his policy for the financial services: greater political control over the Bank of England, another policy straight out of the MAGA playbook. Does he have an original thought?

Fascination with crypto

A few days later he made an appearance at the Zebu Live conference in London, best described as a gathering of crypto zealots. Again, he was mimicking his hero Trump, who has embraced the world of digital assets and crypto, making sure he and his family profit handsomely from it, not least by lessening the regulatory oversight of the sector.

Farage gave a lot away at the Zebu event, lauding the lack of transparency and accountability of crypto assets: “Being in control of your own money, making your own decisions, free from authoritarian government. Crypto is the ultimate freedom of the 21st century and debanking taught me that for life”, a reference to his own dispute with Coutts in 2023.

Do we really want a parallel financial world where the already rich, and often disreputable, can make themselves richer with no accountability?

I continue to shudder at the way the super-rich never stop at seizing any opportunity to make themselves richer, while many, like Farage, build a narrative to appeal to those who feel society has left them behind, by demonising and dehumanising people who often have even less themselves or are even more vulnerable.

This obsession with deregulation makes me fear for the wider good of society. Let’s be clear, the sort of self-regulation Reform envisages would be a charter for spivs, charlatans and crooks. We have tight regulation in financial services because there have been too many examples of the unscrupulous using lax regulation to exploit people.

Scandal is never far away

I have reported too many major financial scandals to know that light touch regulation is always a failure. Payment protection insurance, endowment insurance and personal pensions mis-selling and the most recent, the £11bn car finance scandal, are just a glimpse of the scandals that explain why we have tight, compulsory regulation. Lessening that is very hard to justify if you believe people need protecting from those who would take advantage of them.

Is the current statutory regime occasionally over-prescriptive? Probably. But rarely does a year go by without some necessary intervention by a regulator to protect customers show why an empowered, independent regulator is essential. It creates a level playing field which protects the majority of ethical, honest businesses, as well as consumers.

What Reform wants to do will open up our financial services sector to crooks and charlatans who will exploit people and businesses. They have nothing to offer the City, the financial services sector or the country.

The enthusiasm sweeping the City of London and the wider financial services sector following the Chancellor of the Exchequer’s Mansion House speech on Tuesday evening, which came hard on the heels of that morning’s announcements at an event in Leeds of a wide ranging package of changes to financial services regulation, is palpable.

It makes me nervous. Why?

Quite simply, because I have been writing about financial services for long enough to have seen too many deregulatory initiatives end in tears.

There are many positive features among the proposals that have flooded out of the Treasury this week: simplification of listing rules to encourage IPOs, the creation of a captive insurance regime in London and the promise to regulate ESG (Environment, Social and Governance) ratings providers, although the latter is diluted by the dropping of the plans for a UK green taxonomy.

The two areas that make me nervous are the relaxation of some of the regulations put in place after the 2008 financial crisis, especially the clear separation of banks’ wholesale and retail operations and the instance that those in charge of financial institutions demonstrate their competence and probity through the Senior Managers Certification (SMCR) scheme.

‘Tell Sid’ to ‘Break the Chains’

It is the push to persuade retail investors to take more risks with their money by committing their savings to stocks and shares that really starts ringing alarm bells with me.

There are very good reasons why savers should keep a decent proportion of their money in investments that cannot lose their value, such as Cash ISAs or Premium Bonds: it will be there when they need it. The threat that the government should back a promotional campaign to encourage people to put savings – should they have any – into riskier share-based investments should be quashed. It never ends well. We had this nonsense in the 1980s and early 1990s with campaigns to encourage people to buy into privatisations – ‘Tell Sid’ – and then the push to persuade people to leave perfectly good occupational pension schemes and invest in a new breed of private pensions instead – ‘Break the Chains’.

The latter ended in disaster as it unleashed a wave of mis-selling that cost the sector over £12bn to correct. The reputational risks for Rachel Reeves, the government and the sector are enormous.

Unfortunately, the temptation to mis-sell risky investments will be irresistible to some advisers. I have already seen comments claiming that revising the current definition of Consumer Duty to allow a presumption in favour of stock market investments will allow advisers to persuade customers to move money out of interest-bearing accounts. Worrying.

Rachel Reeves needs to stop vacillating over the future of cash ISAs as this breed of less scrupulous adviser is already circling in the hope that the cap will be reduced. Cash ISAs are a perfectly decent, well-advised investment for people who need confidence that their savings will be intact just when they need them.

Stock markets go down – far and fast

Perhaps an advertising campaign should start with reminders of the catastrophic stock market crashes in 1987, 2000 and 2008, as well as the volatility in the wake of Trump’s unpredictable economic policy pronouncements. Yes, markets recover but some people will not be in a position to wait for them to return their money.

The Chancellor’s frantic search for growth must not put people’s savings at risk, nor must it turn a blind eye to the lessons that were learned in the wake the 2008 global financial crisis.

Over the last few weeks it has been a great privilege, and a time-consuming challenge, to review hundreds of entries for the Women in Insurance Awards. The stories are frequently inspiring, often deeply moving and a reminder that in every walk of life women face many barriers to achieving their full potential.

Now in their seventh year, the Women in Insurance Awards are firmly established as the biggest celebration of the achievements of women in the insurance industry. This year they also feel like a bulwark against the growing assault on diversity and inclusion from the ignorant, prejudiced forces of darkness on the far right.

Led by Donald Trump, their determination to destroy the hard-won progress of decades has cowed businesses into retreating from lofty promises to embrace Diversity, Equity and Inclusion (DEI) and deliver lasting change. This corporate cowardice comes as no surprise, as it follows hard on the abandonment by most of the world’s largest financial institutions of commitments to tackle climate change. This started with spurious claims from Republican states that co-ordinated action through initiatives such as the Net Zero Insurance Alliance breached competition law. This was a smoke-screen for climate-change denial, now given further credibility by Trump. No fight, no backbone, just meek submission was the depressing response of most business previously quick to align themselves with the net zero initiatives launched by Mark Carney at COP26,.

Now that contagion of cowardice is infecting corporate responses to the far right’s attacks on DEI. So far, the rush for the exit door does not seem as panicky as it has been over climate change but it is still happening. Bold statements about DEI policies are being watered down or disappearing from company websites. Collectively, executives are taking a lower profiles, although there are many exceptions. In the public sector in the UK, local councils that fell into the grubby hands of Reform in May are purging DEI policies.

In this context, the huge support for the Women in Insurance Awards seems like an act of defiance: a determination to say 1000s in the market believe in diversity and inclusion and understand the great value it delivers.

It is not the only sign that many are drawing a clear line in the sand. Insurance Post’s relaunch of its Diversity and Inclusion in Insurance Awards will seek out those committed to the wider DEI agenda, We will watch carefully those business that support the awards, as well as those conspicuous by their absence. There is a growing list of organisations and networks in the UK insurance market committed to promoting DEI: they deserve support as this is a cause we cannot abandon.

When the winners of the Women in Insurance Awards are revealed at Grosvenor House on 23 October it will a great celebration: it will also be an expression of solidarity in these darker times.

If you doubt the darkness of the clouds that are depending all around us, just pause to reflect on the conversations the insurance and financial services sector was having just two years ago about climate change, ESG (Environment, Social and Governance) and DEI. Would you have imagined where we are today?

Many of us have supported the development of ethical investment strategies since the concept first became mainstream in the 1980s when firms such as Friends Provident promoted a new generation of ethical investment funds. Since then the concept has had various iterations and is now embedded in the Environment, Social and Governance (ESG) strategies of many major financial institutions.

Once, it was almost automatically assumed that spending on weapons had no place in an ethical or ESG investment strategy. Now, we must question that.

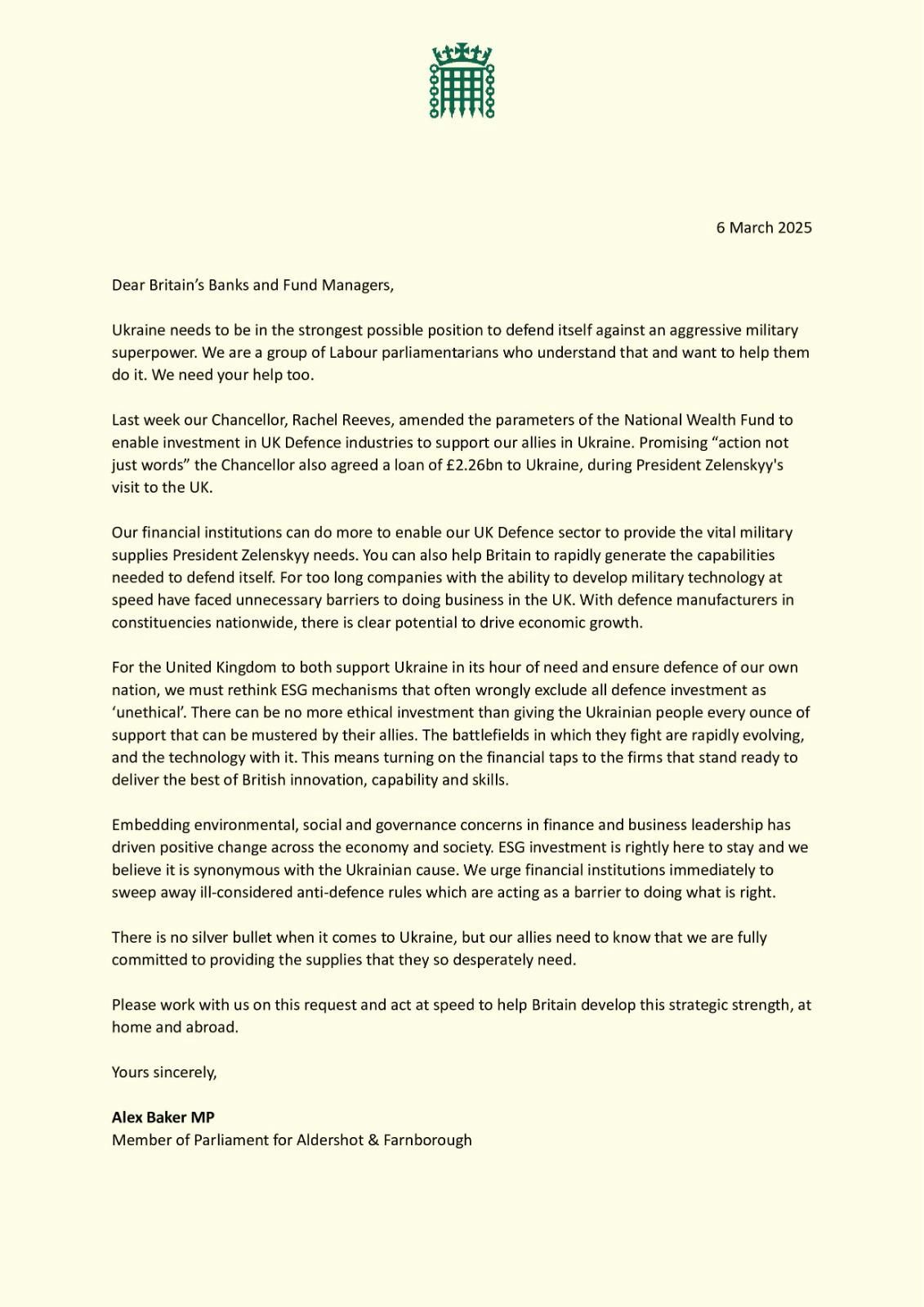

A group of Labour MPs have posed this question to our financial institutions in an open letter published in the Financial Times (below for those unable to access the FT’s content).

Their arguments are compelling, even though they make uncomfortable reading for those of us who hoped – and campaigned – for a more peaceful and safer world. Those hopes have been dashed. We now live in a more dangerous world, one where the threats to freedom, democracy, tolerance, prosperity and the rules-based international order are more acute than any time since the Second World War. Those threats are not theoretical or intellectual, they are violent, brutal and existential.

Sadly, force is going to have to be met with force if the values we so passionately hold are to be protected. No-one should take any pleasure in having to argue this.

What role for our nuclear weapons …?

Of course, this a complex issue. It will be about how we re-arm and where we find the money form. It also brings into the mix our nuclear weapons and the future of NATO.

Again, I find myself in a dilemma, at least on the question of nuclear weapons as I have long campaigned for their abolition. I find myself breathing a sigh of relief that ourselves and France still have a nuclear deterrent, although only France’s can be described as independent as the mistakes of the Thatcher government when replacing Polaris have made us too dependent on America.

One aspect I do find encouraging is the determination of Europe to take greater responsibility for its own security.

… and what role for NATO?

I have never been an enthusiastic Atlanticist. I thought back in the 1970s that a combined European Defence Force should be a key part of an expanding European Union to give Europe a chance of controlling its own destiny, liberated from dependence on the Americans. Then, through NATO, we were part of a world polarised between the West and the Soviet Union, the Russian Empire of its day. A third force (China wasn’t in the picture then) seemed to me to offer a better prospect of avoiding the tensions between the two great power blocks escalating into anything more serious.

Such was my dislike of NATO and distrust of the Americans that when the Liberal Party and the Social Democratic Party merged to create the Liberal Democrats in the late 1980s, I was one of a group of Liberals who opposed including mention of NATO in the preamble to the new party’s constitution, an argument we thankfully won. Europe now has to seize the chance to shape its own destiny, founded on the values previous generations fought for and sacrificed so much to defend. NATO has to become a partnership of two equals if it is to have any relevance in the future. We have to to ready to accept that the current US government may not be prepared to commit to that, reinforcing the need for Europe to move quickly and decisively, embracing UK Prime Minister Kier Starmer’s appeal to a”coalition of the willing”.

That will need huge financial resources which is why we must look to financial institutions to play their part by investing in those companies that are now needed to help re-arm us. If they do not, then what values embedded in the ‘Social’ part of ESG will be left?

As the dark clouds of bigotry and ignorance emanating from the White House cast their lengthening shadows across the corporate world, we all have a duty to support those trying to hold the line and preserve Diversity, Equality and Inclusion (DEI) initiatives.

The last few weeks have seen major businesses retreat from previously proudly proclaimed DEI policies, clearly following the lead from President Trump and his emboldened “anti-woke” stormtroopers. The sackings of top black and female military commanders can surely leave no-one in any doubt about the true motivations for these savage actions.

To see some of the world’s largest and most powerful businesses fall in behind this is shocking but not surprising.

The collapse of the many initiatives around the COP 26-inspired Glasgow Financial Alliance for Net Zero (GFANZ) showed how easily intimidated major firms are when political sabres are rattled in their direction. The rapid withdrawal of insurers, banks and asset managers from GFANZ’s initiatives showed a shocking degree of corporate cowardice. They meekly caved in in the face the threats of legal action over competition law. These were crudely contrived and entirely specious. We all know the real motivation of the Republican attorneys-general was climate change denial.

Some of the same suspects – Goldman Sachs, Blackrock, Wells Fargo, Citibank and Morgan Stanley among others – have been quick to abandon or water-down their DEI policies at Trump’s behest. They have been joined by two of the big four global consultancies – Deloitte and KPMG. Other financial, consulting, service and manufacturing giants will no doubt follow.

But there is hope.

Deloitte UK has distanced itself from this spineless retreat, as has McDonald’s UK operation. Others are hopefully quietly doing the same. I do not doubt the huge challenges the UK and European executives of these global businesses face in trying to hold the line against what must be uncomfortable pressure from their US counterparts and bosses.

That is why we must do everything we can to support them and help them hold the line on DEI. Some may say why? There are many answers to that question: fairness and justice leap out. But businesses benefit from having a more diverse, representative workforce. Supporting DEI is a win-win for everybody.

More members of the House of Lords – 38 more to be precise – were named by Prime Minister Kier Starmer just before Christmas. British politics takes this enormous patronage in its stride, but it shouldn’t.

The House of Lords is an affront to democracy. It has no place in any democratic institution as we move into the second quarter of the 21st century. Adding to its 800 plus unelected members has little justification beyond short-term political expediency. Labour’s pleas – 30 of the new peers are Labour – that it needs to balance the years of the Conservatives stuffing the House of Lords with their supporters is a very weak argument, especially when it is not accompanied by a plan for meaningful reform.

Labour will point to its commitment to bring to an end to most outrageous anachronism by expelling the remaining 92 hereditary peers sometime next year, but that barely touches to problem of the huge democratic deficit of having an unelected second chamber.

There is talk of bringing in a compulsory retirement age of 80 but that would remove no more than another 15-20 members, still leaving it with over 730 active peers.

We need to go further, faster.

Clearly, in the long term a complex modern democracy needs a elected second chamber, although whether one is required at all should be the starting point for any debate. There are many views on how reform might be achieved and there should be a thorough, deliberative and inclusive process so that we emerge with a solution that will enhance our democratic processes and constitution – perhaps it might even act as a catalyst for putting our constitution in writing.

In the meantime, we need to find a way of cutting the House of Lords down to size, especially now it doesn’t have the burden of scrutinising European legislation since we left the European Union. Removing the 25 Lords Spiritual – representative of only one denomination of one religion – would be another step in the right direction but would still leave it with over 700 members, larger than the democratically elected House of Commons.

My solution to cut it down to size sooner would be to impose a limit on how long people can serve.

We should aim for a maximum ten year term for all peers. This could be introduced gradually, perhaps starting with all those who have already served, say, 15 years and reducing that year-by-year until reaching a maximum term of ten years. By the time we have reached that – which would be just after the end of this Parliament if it goes its full term – we might have elected a government with a mandate to complete the job with a plan for a new, democratically elected second chamber. We can only hope.

Change its name now

One reform that should be immediate is a change of name. How have we got this far into the 21st century with a gender-specific name for one of our main Parliamentary institutions? It should be changed to the House of Peers immediately. No feeble excuses about tradition, history, the need to change a few signs acceptable. Get on with it.